Mathematical model for resistance and optimal strategy

Résumé

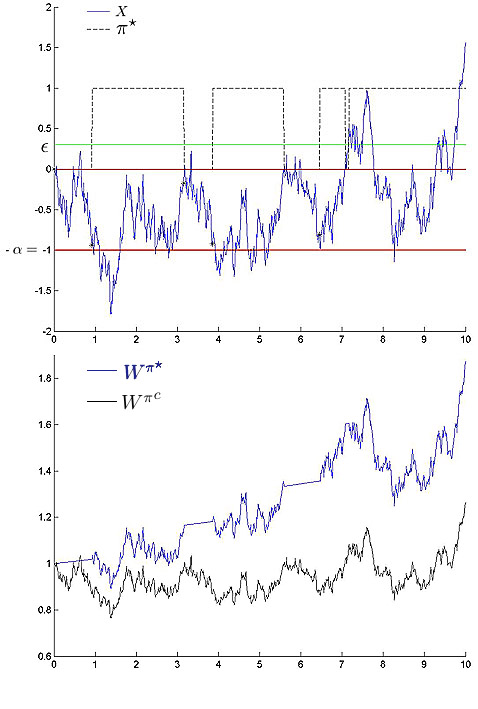

We propose a mathematical model for one pattern of charts studied in technical analysis: in a phase of consolidation, the price of a risky asset goes down $\xi$ times after hitting a resistance level. We construct a mathematical strategy and we calculate the expectation of the wealth for the logaritmic utility function. Via simulations, we compare the strategy with the standard one.

Domaines

Probabilités [math.PR]

Fichier principal

TechnicalAnalysisHAL.pdf (202.59 Ko)

Télécharger le fichier

technicalcourbes.jpg (88.92 Ko)

Télécharger le fichier

TechnicalAnalysisHAL.pdf (202.59 Ko)

Télécharger le fichier

technicalcourbes.jpg (88.92 Ko)

Télécharger le fichier

{kind=link}

Origine : Fichiers produits par l'(les) auteur(s)

Format : Autre

Loading...